{kind=link}

The rise of neobanks has reshaped financial services in ways that would have seemed unlikely just a decade ago. Digital-first, branchless, API-driven, and customer-obsessed—these institutions have unlocked access, convenience, and speed. But along with innovation comes a heavy regulatory burden. Unlike traditional banks, neobanks often operate across borders, rely on third-party infrastructure, and evolve rapidly. That combination makes compliance not just a requirement, but a moving target.

Many founders initially treat compliance as a checkbox—something to “solve” once licensing is secured. In reality, compliance is an ongoing system, not a one-time project. The difference between neobanks that scale smoothly and those that stall or face regulatory action often comes down to how well they embed compliance into their operations.

Below are five proven compliance strategies that go beyond theory. These are approaches that have been tested in real environments—adapted, refined, and made practical for fast-moving fintech teams.

strategy 1: build compliance into product design (compliance-by-design)

One of the most effective strategies is also the most overlooked: embedding compliance directly into product architecture from day one. Instead of treating regulatory requirements as an afterthought, successful neobanks treat them as core product features.

Why this works:

When compliance is bolted on later, it creates friction. You end up with patchwork solutions, duplicated data flows, and inconsistent enforcement. Compliance-by-design avoids this by aligning legal, technical, and operational requirements at the blueprint stage.

Key components:

- integrated KYC flows during onboarding

- automated AML monitoring tied to transaction engines

- real-time sanctions screening APIs

- audit logs embedded in system architecture

- role-based access control for internal tools

Example workflow comparison:

| Aspect | Traditional Approach | Compliance-by-Design Approach |

|---|---|---|

| KYC Integration | Separate vendor after launch | Built into onboarding flow |

| Transaction Monitoring | Batch-based, delayed | Real-time event-driven alerts |

| Audit Trails | Manual logging | Automatic immutable logs |

| Regulatory Reporting | Periodic manual reports | Auto-generated from live data |

Practical implementation tips:

- involve compliance officers in product sprints

- map regulatory requirements to user journeys

- design APIs with compliance checkpoints

- use event-driven architecture to trigger alerts

A subtle but important shift happens when teams adopt this strategy. Engineers stop asking “how do we add compliance?” and start asking “how do we build this feature in a compliant way?”

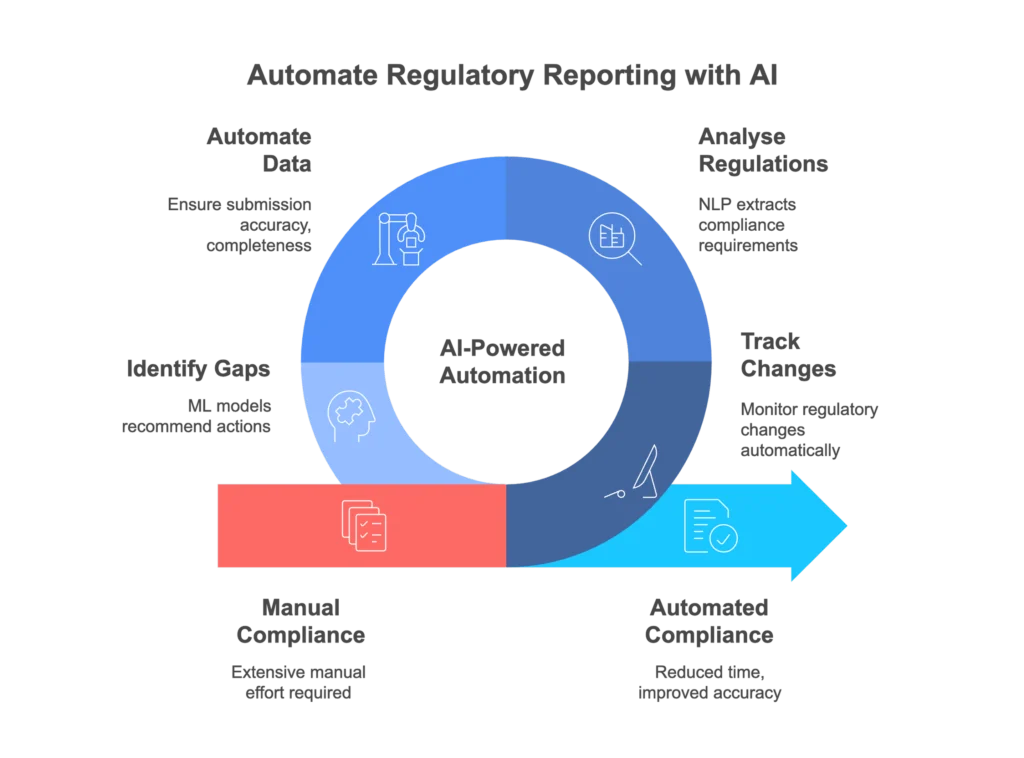

strategy 2: automate regulatory monitoring and reporting

Manual compliance processes don’t scale. As transaction volumes grow, relying on human review alone becomes both inefficient and risky. Automation is no longer optional—it’s foundational.

But automation doesn’t just mean replacing humans. It means designing systems that continuously monitor, flag, and report issues with minimal latency.

Core areas to automate:

- transaction monitoring (AML)

- suspicious activity reporting (SAR)

- sanctions list updates

- customer risk scoring

- regulatory filings

A typical automation stack might look like this:

| Layer | Function | Example Output |

|---|---|---|

| Data Ingestion | Collect transaction data | Raw transaction logs |

| Rules Engine | Apply AML rules | Flagged transactions |

| Machine Learning Layer | Detect anomalies | Risk scores |

| Reporting Module | Generate reports | SAR/STR reports |

| Audit System | Record decisions | Compliance logs |

Benefits of automation:

- faster detection of suspicious behavior

- reduced human error

- consistent rule enforcement

- lower operational costs

- easier audits

However, automation must be carefully calibrated. Overly aggressive rules can generate false positives, overwhelming compliance teams. Too lenient, and real risks slip through.

A balanced approach involves:

- periodic rule tuning

- feedback loops from analysts

- hybrid systems combining rules + ML

- clear escalation paths

strategy 3: adopt a risk-based compliance framework

Not all customers, transactions, or regions carry the same level of risk. A one-size-fits-all compliance approach wastes resources and reduces effectiveness.

A risk-based framework prioritizes attention where it matters most.

Core principle:

Allocate compliance resources proportionally to the level of risk.

This involves categorizing:

- customers (low, medium, high risk)

- geographies (based on regulatory risk)

- transaction types (e.g., crypto, cross-border)

- business partners (vendors, APIs)

Example risk segmentation table:

| Category | Low Risk Example | Medium Risk Example | High Risk Example |

|---|---|---|---|

| Customer Type | Salaried individual | Small business owner | Politically exposed person |

| Geography | OECD countries | Emerging markets | Sanctioned jurisdictions |

| Transactions | Domestic transfers | Cross-border payments | Large crypto transfers |

| Behavior | Stable patterns | Occasional anomalies | Frequent unusual activity |

Once categorized, compliance measures can be tailored:

- simplified due diligence for low-risk users

- enhanced due diligence (EDD) for high-risk users

- transaction limits based on risk profile

- increased monitoring frequency

Advantages:

- more efficient use of resources

- improved detection of real threats

- better customer experience for low-risk users

Challenges:

- requires accurate data

- needs continuous updating

- depends on strong governance

A well-executed risk-based model becomes a dynamic system. It evolves as new risks emerge, rather than remaining static.

strategy 4: establish strong third-party and vendor compliance controls

Neobanks rarely operate in isolation. They depend heavily on third-party providers for:

- payment processing

- identity verification

- cloud infrastructure

- card issuing

- fraud detection

This interconnected model introduces a critical vulnerability: third-party risk.

Regulators increasingly expect neobanks to ensure that their vendors meet the same compliance standards.

Key elements of vendor compliance:

- due diligence before onboarding

- contractual compliance obligations

- ongoing performance monitoring

- incident reporting requirements

- exit strategies for non-compliant vendors

Vendor risk assessment framework:

| Criteria | Evaluation Method | Risk Indicator |

|---|---|---|

| Regulatory Status | Licensing verification | Unlicensed provider |

| Data Security | Security audits | Weak encryption practices |

| Compliance History | Past violations | Regulatory penalties |

| Operational Stability | Financial health checks | High failure risk |

| Geographic Exposure | Jurisdiction analysis | High-risk regions |

Practical steps:

- maintain a centralized vendor registry

- conduct annual compliance reviews

- integrate vendor APIs with monitoring systems

- require SOC 2 / ISO certifications where applicable

An often-overlooked point: compliance responsibility cannot be outsourced. Even if a third party fails, regulators hold the neobank accountable.

strategy 5: build a compliance-first culture across the organization

Technology and frameworks are only part of the equation. Culture plays an equally critical role.

In many organizations, compliance is seen as a blocker—a department that slows things down. In high-performing neobanks, compliance is treated as a strategic enabler.

Characteristics of a compliance-first culture:

- leadership actively promotes compliance values

- employees understand regulatory responsibilities

- cross-functional collaboration is encouraged

- transparency is prioritized

- mistakes are reported without fear

Training structure example:

| Level | Training Focus | Frequency |

|---|---|---|

| New Employees | Basic compliance principles | Onboarding |

| Product Teams | Compliance in product design | Quarterly |

| Operations Staff | AML/KYC procedures | Monthly |

| Leadership | Regulatory updates | Bi-annually |

Ways to reinforce culture:

- regular compliance workshops

- internal audits and feedback loops

- clear documentation and playbooks

- recognition for compliance excellence

- open communication channels

When compliance becomes part of everyday thinking, organizations move faster—not slower. Decisions are made with clarity, reducing rework and risk.

integrated compliance maturity model

To understand how these strategies come together, it helps to look at compliance maturity levels.

| Level | Characteristics | Risk Level |

|---|---|---|

| Level 1 | Reactive, manual processes | High |

| Level 2 | Basic automation, siloed systems | Moderate |

| Level 3 | Integrated systems, risk-based approach | Lower |

| Level 4 | Fully automated, real-time compliance | Minimal |

| Level 5 | Predictive, AI-driven compliance ecosystem | Optimized |

Most successful neobanks operate at Level 3 or above. The goal is not perfection, but continuous improvement.

common pitfalls to avoid

Even with strong strategies, certain mistakes repeatedly surface:

- over-reliance on manual processes

- ignoring regulatory changes

- poor data quality

- lack of internal communication

- underestimating third-party risks

A quick diagnostic checklist:

| Question | Yes/No |

|---|---|

| Are compliance checks integrated into product flows? | |

| Is transaction monitoring automated in real time? | |

| Do you use risk-based customer segmentation? | |

| Are vendors regularly audited for compliance? | |

| Is compliance training ongoing across teams? |

If multiple answers are “No,” there’s room for improvement.

future trends shaping neobank compliance

Looking ahead, compliance will become even more complex—and more technology-driven.

Key trends:

- AI-powered fraud detection

- real-time global regulatory reporting

- increased scrutiny on crypto transactions

- stricter data privacy regulations

- open banking compliance frameworks

Emerging technologies:

| Technology | Compliance Impact |

|---|---|

| Artificial Intelligence | Advanced anomaly detection |

| Blockchain | Transparent audit trails |

| RegTech Platforms | Automated regulatory updates |

| API Monitoring | Real-time compliance validation |

Neobanks that embrace these tools early will have a significant advantage.

conclusion

Compliance is often viewed as a constraint. In reality, it can be a competitive advantage. Neobanks that integrate compliance into their DNA—through design, automation, risk management, vendor oversight, and culture—are better positioned to scale sustainably.

The five strategies outlined here are not theoretical ideals. They are practical, proven approaches that align with how modern financial systems operate. When implemented correctly, they reduce risk, improve efficiency, and build trust with regulators and customers alike.

The real takeaway is simple: compliance works best when it’s not treated as a separate function, but as a core part of how the business operates.

frequently asked questions

- why is compliance more challenging for neobanks than traditional banks?

Neobanks operate digitally, often across multiple jurisdictions, and rely heavily on third-party providers. This creates a more complex regulatory environment compared to traditional banks with localized operations. - can small neobanks afford advanced compliance systems?

Yes, many RegTech solutions are scalable and offered as SaaS. Smaller neobanks can start with modular tools and expand as they grow. - how often should compliance systems be updated?

Continuously. Regulatory requirements change frequently, and systems should be reviewed at least quarterly, with real-time updates where possible. - what is the biggest compliance risk for neobanks?

One of the biggest risks is inadequate transaction monitoring, especially as volumes grow. This can lead to missed suspicious activity and regulatory penalties. - is automation enough to ensure compliance?

No. Automation is essential but must be complemented by human oversight, governance, and regular audits. - how can neobanks stay ahead of regulatory changes?

By using RegTech platforms, maintaining close relationships with regulators, and having dedicated compliance teams that monitor global regulatory developments.