{kind=link}

Last month, I got a notification from my bank at 2:47 AM. A transaction attempt from somewhere in Eastern Europe. I hadn’t traveled anywhere. My card was sitting right there on my nightstand.

What followed was a frantic 20-minute call with customer support, a temporary account freeze, and an eventual refund — but the whole experience shook me. Because here’s the thing: I thought I was being careful. Strong password, two-factor auth, the works. And yet something still slipped through.

That experience sent me down a rabbit hole of researching how banks are actually fighting back against this stuff. What I found was genuinely fascinating — and honestly, a little reassuring. The security game is changing fast, and the trends driving that change are worth understanding, whether you’re a regular banking customer or someone working in fintech.

Let’s get into it.

1. Behavioral Biometrics Are Replacing Passwords (Quietly)

You know how your phone learns your typing rhythm? Banks are doing something similar, but at a much deeper level.

Behavioral biometrics is the practice of tracking how you interact with your banking app — not just who you say you are. This includes things like:

- How fast you type your PIN

- The angle you hold your phone at

- How hard you press the screen

- The way you scroll through transaction history

I first heard about this from a friend who works at a mid-sized fintech company. She mentioned that their fraud detection system flagged a legitimate user once because he was typing unusually slowly — turned out he had a hand injury that week. The system caught the behavioral anomaly and triggered a verification step.

That’s how granular this stuff is now.

Why it matters: Stolen passwords are basically useless if the behavioral pattern doesn’t match. A hacker sitting in another country isn’t going to replicate the exact way you tap your phone.

Banks like HSBC and Barclays have been deploying behavioral biometric layers for a few years now. Neobanks like Revolut and Monzo are also building similar systems into their apps.

The practical takeaway for you? Keep your apps updated. These biometric systems improve with each update, and an outdated app might be missing the latest fraud-detection layer entirely.

2. AI-Powered Real-Time Transaction Monitoring

The old way banks detected fraud was essentially reactive — they’d notice something was wrong after the damage was done, then investigate. Not ideal when someone’s draining your account in real time.

Now, AI models are analyzing transactions as they happen, in milliseconds.

Here’s a simplified version of what these systems do:

| What They Monitor | Why It Matters |

|---|---|

| Transaction location vs. usual patterns | Catches geographic anomalies |

| Transaction size relative to history | Flags unusual spending spikes |

| Merchant category patterns | Detects out-of-character purchases |

| Time of day and frequency | Identifies scripted or bot-driven activity |

| Device and IP metadata | Spots new or suspicious access points |

When I looked into the 2:47 AM incident I mentioned earlier, my bank confirmed that their AI system had flagged the transaction before it even processed — and that’s why I got the alert in real time rather than discovering it on my statement.

The models are trained on millions of transactions and continuously retrained as fraud patterns evolve. What’s clever is that they’re not just looking for “bad” patterns — they’re looking for deviation from your specific normal.

One mistake I see people make: ignoring those weird little push notifications from their banking apps. Don’t. That’s your AI security layer trying to talk to you.

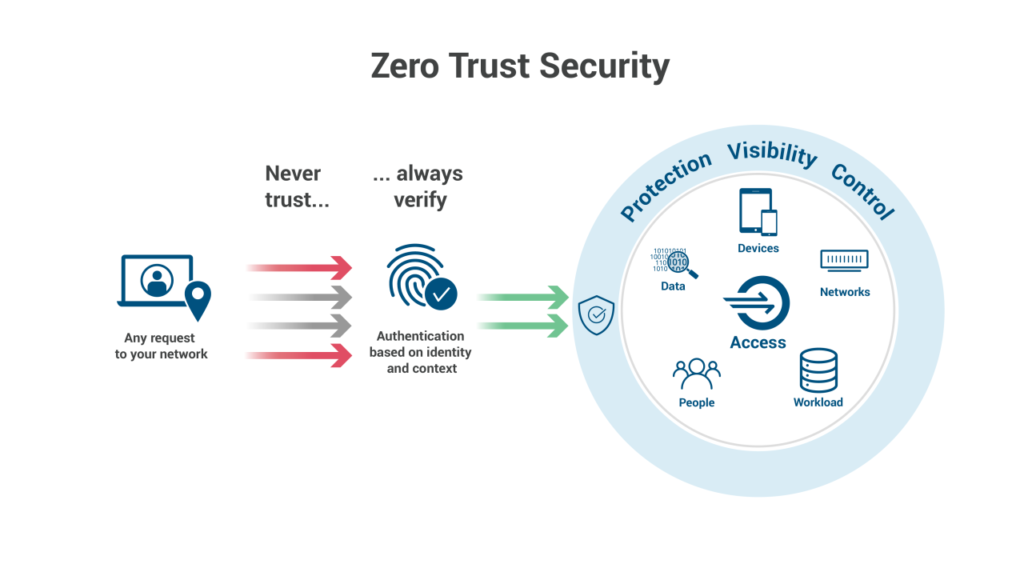

3. Zero Trust Architecture Is Finally Going Mainstream in Banking

“Never trust, always verify.” That’s the core idea behind Zero Trust — and it’s a pretty radical departure from how legacy banks used to think about security.

Old model: Get past the login screen, and you’re basically trusted to roam around. Like getting a wristband at a theme park — one check, then free access everywhere.

Zero Trust model: Every action, every click, every API call gets verified independently. No implicit trust based on previous authentication.

For online banking, this translates to things like:

- Re-verification prompts when moving large sums

- Device trust scoring (is this the same device you always use?)

- Session timeouts that adapt based on risk level

- Micro-segmentation of banking systems so a breach in one area doesn’t cascade

I spoke with a security consultant who works with regional banks on this. He told me something that stuck: “Most breaches don’t happen at the front door. They happen when someone’s already inside and moving laterally.” Zero Trust is designed specifically to stop that lateral movement.

For neobanks especially, this is a critical architecture choice. They’re building from scratch, which means they can bake Zero Trust in from day one rather than retrofitting it onto 30-year-old infrastructure.

If your bank still logs you in once and leaves you in for 6 hours without any re-verification, that’s worth noting. It’s not 2015 anymore.

4. Deepfake Detection and Voice Authentication Threats

This one caught me completely off guard when I first read about it.

Social engineering — tricking humans rather than hacking systems — has always been a threat. But deepfake technology has turbocharged it in ways that feel almost cinematic.

There have been documented cases where criminals cloned the voice of a CEO to authorize wire transfers. And that same tech is now being pointed at bank call centers.

Imagine someone calls your bank’s customer service line with a cloned version of your voice, claiming to need an urgent transfer. The agent, trained to verify by voice, hears what sounds convincingly like you.

Banks are responding in a few ways:

Liveness detection — For video-based verification (increasingly common for opening accounts or approving large transfers), systems now check for micro-movements, blink patterns, and depth cues that deepfakes struggle to replicate.

Voice print anomaly detection — AI models trained to detect the subtle artifacts left by voice synthesis tools. Not perfect, but improving rapidly.

Context-aware verification — If “you” call asking for a transfer but your app shows you actively logged in and doing something else at the same time, that’s a red flag the system can catch.

The honest truth is this is a cat-and-mouse game, and deepfakes are evolving fast. But banks that run regular security audits on their authentication systems are catching these vulnerabilities before attackers can exploit them.

What you can do: Set up a verbal passphrase or security word with your bank that you’d include in any legitimate call. It’s old-school, but it works.

5. Open Banking APIs Are Creating New Attack Surfaces — And New Defenses

Open banking is genuinely exciting. The idea that third-party apps can securely connect to your bank with your permission, pulling in your data to power budgeting tools, investment apps, lending services — it’s transformative.

But every API endpoint is also a potential entry point for attackers.

Here’s a scenario that’s played out in real fraud cases:

- User grants a sketchy “budgeting app” access to their bank via open banking

- That app, poorly secured or outright malicious, leaks the OAuth token

- Attacker uses the token to access account data or initiate transfers

The security community calls this “supply chain risk” in the API world — you’re only as secure as the third parties you connect to.

What’s being done about it:

| Defense Mechanism | How It Works |

|---|---|

| OAuth 2.0 with PKCE | Prevents token interception during authorization |

| Granular permission scopes | Users can grant “read only” without enabling transfers |

| Token expiration and rotation | Short-lived tokens that auto-expire reduce risk window |

| API rate limiting | Prevents automated scraping or brute-force attacks |

| Third-party app vetting | Banks increasingly audit apps before allowing API access |

Regulators are also stepping in — PSD2 in Europe, for example, has strict requirements around Strong Customer Authentication (SCA) for API-connected services.

My personal rule: I audit my connected apps every few months. Go into your banking app settings and look at what third-party services have access. You might find an old app you forgot about from three years ago still sitting there with live permissions.

Revoke anything you don’t actively use. It takes two minutes.

6. Quantum-Resistant Encryption Is Moving from Theory to Implementation

Okay, this is the one that sounds like science fiction but really isn’t.

Current encryption standards (RSA, ECC) that protect your banking data are theoretically vulnerable to quantum computers. Not today’s quantum computers — they’re nowhere near powerful enough — but potentially within the next decade.

The concern is something called “harvest now, decrypt later.” Sophisticated attackers could be collecting encrypted banking data right now, banking on the fact that quantum computers will eventually be powerful enough to crack the encryption retroactively.

It sounds paranoid. But governments and major financial institutions aren’t treating it as paranoia — they’re treating it as a planning horizon.

NIST (the National Institute of Standards and Technology) finalized its first set of post-quantum cryptographic standards in 2024. Major banks and payment networks have started the slow, expensive process of upgrading their cryptographic infrastructure.

For context on how seriously this is being taken: JPMorgan, IBM, and several European central banks have active quantum-readiness programs. The Bank for International Settlements published guidance specifically on this.

What this means practically for you right now: Honestly, not much you need to do today. But it’s worth knowing that if your bank is still using decade-old encryption protocols and hasn’t published anything about their modernization roadmap, that’s worth raising an eyebrow at.

The banks doing this right are the ones running comprehensive security audits that include cryptographic assessments — not just checking boxes on compliance forms.

Common Mistakes People Still Make (And Banks Aren’t Helping)

Despite all this sophisticated security infrastructure, the weakest link is still usually the human side.

Here’s what I see constantly:

Reusing passwords across banking and other sites. Even if your bank has amazing security, if you use the same password on a breached forum, you’re exposed.

Ignoring app update prompts. Security patches live in those updates. Running a 6-month-old version of your banking app is genuinely risky.

Granting excessive permissions. Third-party apps asking for full account access when they only need to read your balance — say no, or look for an alternative.

Clicking links in banking emails without verifying. Phishing is still how a huge proportion of banking fraud starts. When in doubt, open your app directly rather than clicking any link.

Not setting up account alerts. Every major bank lets you set real-time alerts for transactions above a certain amount. If you haven’t done this, do it today.

A Quick Note on Neobanks vs. Traditional Banks

I get asked this a lot: are neobanks less secure?

It’s nuanced. Traditional banks have deeper pockets and longer track records. But they also have legacy infrastructure that’s genuinely hard to secure.

Neobanks are building on modern stacks, which makes it easier to implement the trends above — behavioral biometrics, Zero Trust, quantum-ready encryption — from the ground up. But they’re also younger, sometimes less battle-tested, and regulatory oversight varies by region.

The security audit practices a neobank runs tell you a lot about how seriously they take this stuff. Look for published penetration testing results, third-party audit reports, and bug bounty programs. If a neobank can’t point you to any of that, ask why.

Final Thoughts

The 2:47 AM alert I mentioned at the start? That was actually security working correctly. The system caught something, flagged it, and protected me. I was shaken, but I wasn’t robbed.

That’s the goal of all six trends above — not just keeping pace with attackers, but getting ahead of them. Behavioral biometrics, AI monitoring, Zero Trust, deepfake defenses, API security, and quantum-resistant encryption aren’t buzzwords. They’re the actual architecture of modern banking security.

The best thing you can do as a user is stay informed, audit your own habits, and pay attention when your bank’s security systems try to communicate with you. They’re doing more than you probably realize.

Also worth reading: 10 Smart Neobank Digital Wallet Security Audits Tips for Dummies — a solid breakdown of practical audit steps anyone can follow, even without a technical background.