{kind=link}

I still remember sitting in a meeting with a compliance officer from a mid-sized bank who’d just come out of a brutal regulatory review. Auditors had flagged three critical gaps in their digital controls — not because the bank was doing anything shady, but because their audit process was stuck in 2015. Paper checklists. Manual reconciliations. Excel spreadsheets that took two days to compile.

That conversation stuck with me. Because the reality is, most banks — even well-run ones — are still using tools that are genuinely not built for the speed, volume, or complexity of modern banking. And when something goes wrong (a data breach, a compliance gap, a fraud event), the question isn’t “why did this happen?” It’s “how did we not catch this sooner?”

This piece is about the audit tools that actually make a difference — the ones that help banks move from reactive firefighting to proactive control. I’ve seen these tools in action across fintech implementations, neobank audits, and traditional banking environments. Here’s what’s worth your attention.

1. Continuous Transaction Monitoring Platforms

If your fraud or compliance team is still running batch reports at end-of-day, you’re essentially looking at yesterday’s news while today’s problems pile up.

Continuous transaction monitoring tools — like NICE Actimize, FICO TONBELLER, or Oracle Financial Services Anti Money Laundering — watch every transaction in real time and flag anomalies as they happen. What makes these genuinely powerful isn’t just speed; it’s the behavioral baseline they build over time. They learn what “normal” looks like for each customer or account type, and anything outside that pattern gets surfaced immediately.

One thing most people don’t realize: these platforms are also increasingly being used for internal audit purposes, not just fraud detection. Internal teams can use them to verify that transaction approval workflows are being followed consistently across branches or systems.

Common mistake: Banks often deploy these tools but don’t tune the thresholds properly. Out-of-the-box sensitivity settings generate so many false positives that teams start ignoring alerts — which defeats the entire purpose. Spend time calibrating during the first 90 days.

2. Automated Regulatory Compliance Software

Keeping up with regulatory changes — BASEL III, AML directives, GDPR, local central bank requirements — is practically a full-time job on its own. Add the operational work of documenting compliance and you’ve got a team that’s permanently underwater.

Tools like MetricStream, Riskonnect, and LogicGate are purpose-built to automate compliance tracking and workflow management. They map regulations to specific internal controls, assign ownership, and track status in a central dashboard. When a regulation changes, you can see exactly which controls are affected and what needs updating.

What I find underrated about these platforms is their audit trail functionality. Every action, update, and sign-off is logged automatically. During an external audit, you’re not scrambling to prove what happened — you just pull the report.

If you’re exploring how neobanks handle compliance audits differently from traditional banks, this breakdown of neobank digital wallet security audits is worth reading alongside this piece.

3. Data Analytics and Visualization Tools for Audit Teams

Let me be direct about something: most audit teams are not data scientists. They shouldn’t need to be. But they absolutely need to be able to interrogate large datasets without depending on IT to run every query.

That’s where tools like ACL (now Galvanize/Diligent), IDEA Data Analysis, and even well-configured instances of Tableau or Power BI come in. These let auditors run sampling, outlier detection, and population analysis on their own — without writing SQL from scratch.

I’ve watched an auditor at a regional bank use ACL to analyze two years of expense claims in about 45 minutes — something that used to take their team two weeks manually. They found a pattern of split transactions designed to stay below an approval threshold. Not a massive fraud, but exactly the kind of thing that slips through traditional sampling.

Pro tip: Start with the data you already have before buying new software. A lot of banks already have Tableau or Power BI licenses sitting unused in IT. Get your audit team trained on those before committing to a dedicated audit analytics platform.

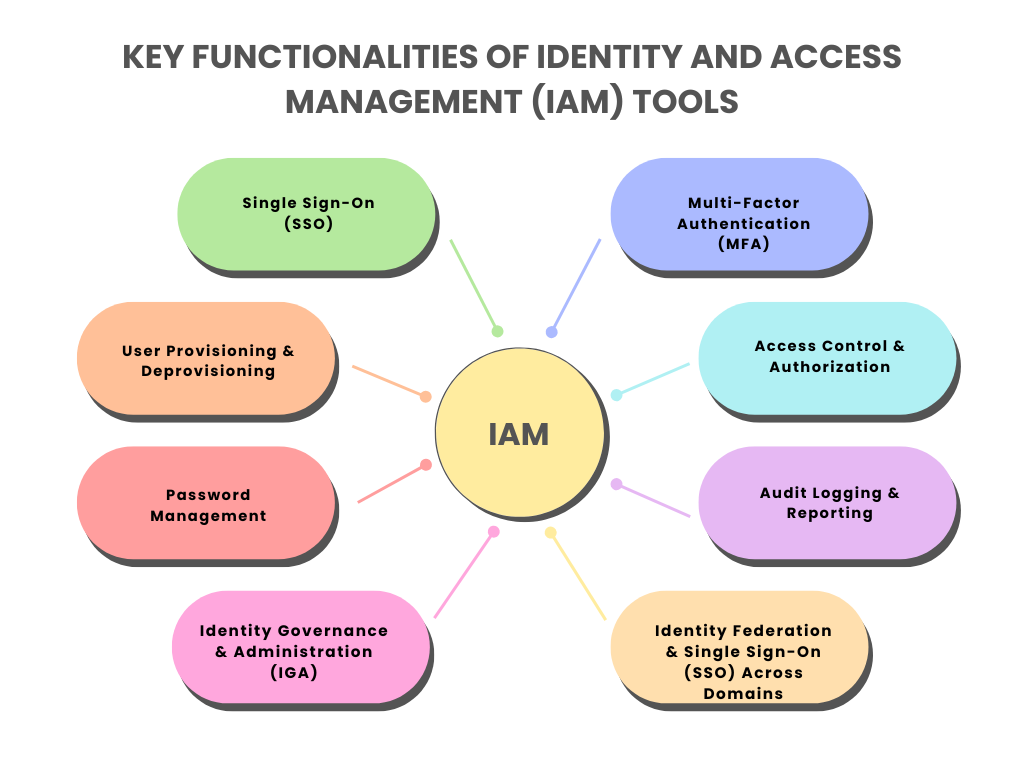

4. Identity and Access Management (IAM) Audit Tools

Here’s a scenario that happens more than banks want to admit: an employee moves to a different department, but their old system access never gets revoked. Six months later, they still have read access to records they have no business seeing. It’s not malicious — it’s just poor access hygiene.

IAM audit tools like SailPoint, CyberArk, or Saviynt provide a continuous view of who has access to what, track changes over time, and flag when access permissions don’t match job roles. The better platforms include “access certification” workflows where managers periodically confirm that their team members’ access is still appropriate.

From a pure audit standpoint, being able to pull a full access history for any user account — including every permission granted, modified, or removed — is invaluable during both internal reviews and regulatory examinations.

The lesson I keep seeing ignored: don’t wait for a breach to start caring about access control. By the time you’re doing forensic analysis after an incident, it’s already too late.

5. Cybersecurity Vulnerability Assessment Tools

Every bank’s IT audit function needs a way to identify security gaps before attackers do. This doesn’t mean hiring a red team for every review cycle — though that has its place — but having ongoing, automated visibility into your vulnerability landscape.

Tools like Qualys, Tenable (Nessus), and Rapid7 InsightVM continuously scan network infrastructure, applications, and endpoints for known vulnerabilities, misconfigurations, and exposure risks. They score findings by severity and track remediation over time.

What’s especially useful for audit purposes is the historical reporting. You can show regulators or board audit committees a trend line: here’s how many critical vulnerabilities we had six months ago, here’s what we fixed, here’s what we still have open and why. That kind of structured accountability is exactly what examiners want to see.

For banks running digital wallet products or embedded finance services, this resource on neobank security audit practices covers additional cybersecurity checkpoints specific to those environments.

6. AI-Powered Risk Scoring and Predictive Analytics Tools

This one is newer territory, but it’s moving fast and banks that ignore it are going to find themselves behind.

Platforms like Quantexa, Ayasdi (now SymphonyAI), and increasingly in-house implementations using Python/ML pipelines are being used to build predictive risk models that score customers, transactions, or even internal processes for risk in ways that rule-based systems simply can’t replicate.

The shift from rule-based to model-based risk detection is significant. A rule might say “flag any transaction over $10,000 to a new payee.” A model looks at the entire behavioral context — account age, device, location, time of day, transaction velocity — and generates a risk score that’s far more nuanced.

For audit teams, the implication is twofold. First, you can use these tools to improve the quality of what you’re testing. Second, you need to be able to audit the models themselves — making sure they’re fair, accurate, and not producing biased outcomes. Model risk management is its own audit discipline now, and it’s only going to grow.

Here’s a rough sense of how AI-assisted audit coverage compares to traditional approaches across key risk categories:

V

visualize

V

visualize show_widget

https://10341f775c3fc4d8715d0f8095dd992d.claudemcpcontent.com/mcp_apps?connect-src=https%3A%2F%2Fesm.sh+https%3A%2F%2Fcdnjs.cloudflare.com+https%3A%2F%2Fcdn.jsdelivr.net+https%3A%2F%2Funpkg.com&resource-src=https%3A%2F%2Fesm.sh+https%3A%2F%2Fcdnjs.cloudflare.com+https%3A%2F%2Fcdn.jsdelivr.net+https%3A%2F%2Funpkg.com+https%3A%2F%2Fassets.claude.ai&dev=true

(These are illustrative estimates based on industry benchmarks — actual results depend heavily on implementation quality and data availability.)

7. Integrated Audit Management Platforms

Everything above needs somewhere to live. Individual tools are great, but if your fraud alerts are in one system, your compliance tracking is in another, your access reviews are in a third, and your vulnerability reports are in a fourth — you’ve just created a different kind of problem.

Integrated audit management platforms like AuditBoard, TeamMate+ (Wolters Kluwer), and Workiva pull the work together. They manage the entire internal audit lifecycle — risk assessment, audit planning, fieldwork, findings, remediation tracking, and reporting — in a single environment.

The real value shows up at reporting time. When a board audit committee or external examiner asks for a summary of your control environment, you’re not pulling data from six different places and manually assembling a presentation. You export it directly.

One thing worth noting: the best implementation I’ve seen of one of these platforms took about four months to fully configure. Don’t expect plug-and-play. Invest in proper setup, train your team on the workflows, and designate a platform owner who’s responsible for keeping it current.

A Few Mistakes Worth Avoiding

After seeing these tools used well and used badly, a few patterns stand out:

Buying tools instead of fixing processes. Software doesn’t fix broken audit methodology. If your risk assessment process is weak, an expensive platform just automates the same weak output faster.

Under-resourcing implementation. The gap between “we bought this tool” and “we’re actually getting value from it” is almost always a people problem, not a technology problem.

Ignoring integration. Tools that don’t talk to each other create blind spots. When selecting any of the above, ask hard questions about API availability and integration with your existing stack.

Not testing the tools themselves. Audit tools need to be audited. Run periodic checks to make sure your monitoring rules are firing correctly, your data feeds are complete, and your alerts are being reviewed.

What the Best-Run Audit Functions Have in Common

The banks that handle audits well — the ones that sail through regulatory examinations and catch problems early — aren’t necessarily using the most expensive tools. They’re using the right tools consistently, with clear ownership and well-documented processes.

They also treat audit not as a once-a-year checkbox exercise but as an ongoing function that generates real business intelligence. A well-run audit isn’t just about compliance — it’s one of the best ways to understand what’s actually happening inside a complex organization.

If you’re looking to benchmark your current setup, this guide to advanced neobank security audit practices has some useful frameworks that translate well to traditional banking contexts too.

The tools covered here — transaction monitoring, compliance automation, data analytics, IAM, cybersecurity scanning, AI risk scoring, and integrated audit management — aren’t a complete picture of everything modern audit functions use. But they are the seven categories where the gap between leading practice and average practice is most visible right now.

Start with the one that’s furthest behind in your organization. That’s usually where the real risk lives.